Rising costs and plummeting listings — to not point out a world pandemic, report unemployment and recession — didn’t hold first-time residence consumers from the market within the second quarter of 2020.

Ordinarily, in April, because the second quarter of the yr begins, homebuying season is effectively underway, and stock and costs are each rising towards a summer season peak. However the second quarter of 2020 was uncommon, to say the least.

Throughout the nation and among the many most populous metropolitan areas, costs elevated modestly within the second quarter and stock grew to become much more constrained in an already sparse market. Householders who’d been planning to promote reconsidered — although listings ticked up barely in April, they fell sharply in Could and June — and individuals who’d been considering of shopping for, at a minimal, took a beat. However actual property professionals scrambled to implement digital excursions and finalize residence purchases in parking tons, and market individuals, significantly economically safe consumers, cautiously got here out of hiding.

Lured partially by report low mortgage charges, first-time residence consumers made up 35% of current residence gross sales in June, in response to the Nationwide Affiliation of Realtors, the next share than previously a number of years. For first-timers who’ve stability within the COVID-19 financial system, and the wherewithal to abdomen a extremely aggressive market, shopping for can nonetheless make sense.

On this quarterly report, we analyze median incomes within the first-time residence purchaser age vary (25-44) in contrast with itemizing costs among the many 50 most populous metro areas to give you an affordability ratio. Budgeting for a house that prices roughly thrice your annual earnings (an affordability ratio of three.0) has been a rule of thumb for years, however first-time consumers typically must stretch past this to account for greater costs in metro areas and their decrease incomes in contrast with repeat consumers. By weighing the affordability ratio versus residence availability within the largest metro areas, we will get an thought of the circumstances first-time consumers are going through after they got down to develop into householders.

By each quarter-over-quarter and year-over-year modifications, we will get a greater image of the results of the COVID-19 financial system on this yr’s homebuying market. The previous can present perception into chronological market responses to the pandemic — our first-quarter affordability report captured knowledge solely by means of March, only the start of 2020’s atypical spring season. The latter can present how this yr’s second quarter contrasts with related durations in comparatively regular occasions.

Click on right here for the Q1 2020 First-Time Residence Purchaser Metro Affordability Report.

Affordability down total

Homes bought barely extra out of attain for first-time residence consumers in April by means of June, rising nationally from 4.5 occasions first-time residence purchaser earnings within the first quarter to 4.7 occasions within the second, and among the many 50 largest metros from 5.1 to five.2 occasions first-time purchaser earnings. This pattern is anticipated presently of yr. Residence costs rise because the housing market heats up within the late spring and summer season, however incomes don’t rise in an identical seasonal style. If something, we’d’ve anticipated a extra dramatic change, however financial uncertainty on the a part of sellers might have saved steeper record value will increase at bay.

9 of the 50 metros analyzed bucked this pattern and noticed affordability enhance, however barely, typically solely by a fraction of a p.c.

The 5 most inexpensive metros for first-time residence consumers within the second quarter embody Pittsburgh (houses listed at 3.1 occasions first-time purchaser earnings), St. Louis (3.4), Cleveland (3.5), Hartford, Connecticut (3.5), and Buffalo, New York (3.6). The least inexpensive, all in California, embody Los Angeles, topping the record for the second quarter in a row, with houses listed at 12 occasions first-time purchaser earnings; San Diego (9.0); San Jose (8.2); San Francisco (7.6); and Sacramento (6.6).

First-time purchaser steerage: Houses get much less inexpensive in late spring to early summer season, and on this regard, the second quarter of 2020 is not any completely different. First-time consumers who’re economically safe might be able to make up for the rise in residence costs by qualifying for report low mortgage charges. For instance, the month-to-month fee on a $240,000 mortgage at 4.1% curiosity — roughly the typical fee a yr in the past — is $1,160 monthly, with $177,483 in curiosity over the 30-year lifetime of the mortgage. Nevertheless, at at the moment’s fee of three.1%, you’d pay $1,025 monthly and $128,942 in curiosity over the lifetime of the mortgage — almost $50,000 in financial savings, whole, and a $135 month-to-month break in your fee. Use a mortgage calculator to see what the distinction in charges means to your price range.

Unseasonal shortage within the second quarter

Even in years when provide is proscribed, an inflow of houses hits the market in the course of the spring homebuying season. Nationally, stock grew 10% from the primary to the second quarter of 2018, and 6% throughout that interval final yr. However in 2020, nationwide stock dipped, albeit barely, by about 2% quarter-over-quarter.

Half of the biggest metros within the nation noticed a lower in common lively listings from Q1 to Q2, with the biggest quarter-over-quarter declines in Cleveland (-17%), Louisville, Kentucky (-14%), and Memphis, Tennessee (-14%). Nevertheless, different massive metros noticed outstanding will increase: San Jose (+62%), Denver (+47%) and San Francisco (+39%), for instance. These dramatic climbs helped push the typical quarter-over-quarter change among the many largest 50 metros to +4%.

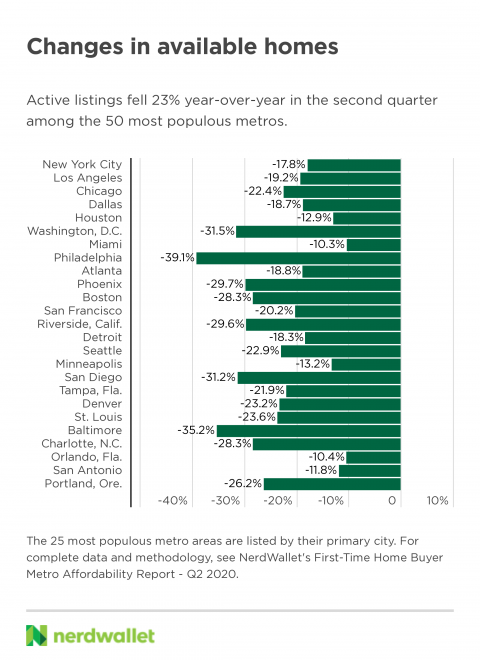

Stepping again to take a look at year-over-year modifications and the way the provision of houses modified from Q2 2019, we discovered stock dropped 23% among the many 50 largest metros, on common, with 21 metros witnessing a lower in accessible houses of 25% or extra. Energetic listings in Las Vegas decreased 8%, the smallest quarterly drop of any metros analyzed and the one one in every of lower than 10%.

We’ve been in a powerful vendor’s marketplace for a while now, as the provision of houses hasn’t saved tempo with demand. Having fewer houses hitting the market in the course of the first months of the pandemic solely stood to worsen the state of affairs. A extremely aggressive market has grown much more so, and consumers with out room to barter may very well be priced out solely.

Click on right here to view a desk that includes lively itemizing knowledge from all 50 metro areas analyzed.

First-time purchaser steerage: For those who’re in any respect unsure about your financial safety this yr and shopping for would imply a rise in total housing prices or go away you with no supply of emergency funds, you could wish to postpone your first residence buy. The low provide of houses means you’re much less prone to discover a residence that checks all of the packing containers in your want record. A lack of earnings, a bout of poor well being or caring for a sick cherished one may very well be overwhelming on high of a down fee, closing prices and the bills related to transferring.

Residence costs rise, as anticipated

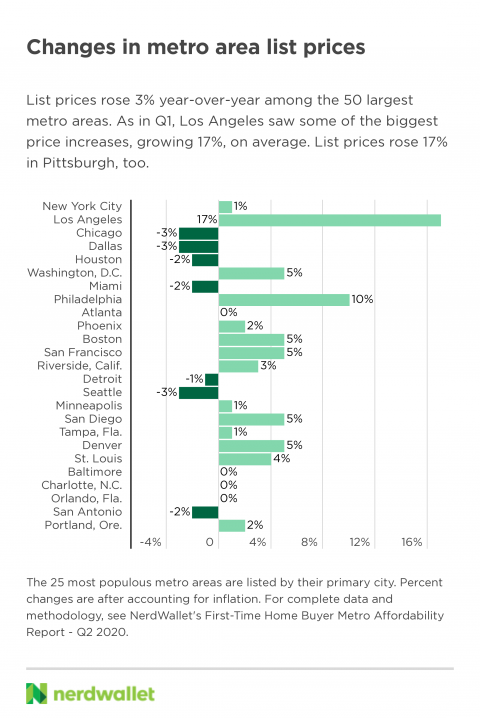

We anticipate costs to rise because the housing market heats up, and if 2020 is sticking to the script in any method, that is it. From the primary quarter to the second, nationwide median record costs grew 7% in 2018 and eight% in 2019. This yr, they grew 7% nationally, and barely much less, 5%, on common, among the many largest metros, quarter-over-quarter.

Yr-over-year development was related, rising about 3%, on common, among the many 50 largest metros, after adjusting for inflation.

This total comparatively unremarkable development in costs is one silver lining for first-time consumers. Having a dramatic scarcity of houses on the market might drive costs up, but it surely doesn’t seem that sellers are itemizing their houses disproportionately greater than final quarter or than presently final yr. That mentioned, record costs are solely a part of the story, and there’s little doubt that the dearth of provide is driving laborious bargaining within the negotiation course of.

Click on right here to view a desk that includes record value knowledge from all 50 metro areas analyzed.

First-time purchaser steerage: The worth you see on a list doesn’t inform the entire story. For those who’re buying in a vendor’s market, be able to act quick with a suggestion and compete with different consumers. It’s possible you’ll find yourself paying greater than record value, so searching for houses listed underneath your max price range provides you with somewhat extra wiggle room if you end up in a bidding battle.

Metro highlight: Cincinnati, Cleveland and Columbus

Ohio has three metro areas in our evaluation. It was additionally among the many first states to start canceling massive occasions, declare a state of emergency and situation statewide restrictions to sluggish the unfold of COVID-19. These components might have performed a task in modifications within the native housing markets.

Cincinnati, Cleveland and Columbus have been a number of the extra inexpensive populous metros within the second quarter, with residence costs averaging 4.7, 3.5 and 4.5 occasions the median first-time residence purchaser earnings, respectively. Even so, all three confirmed rising costs in contrast with the identical interval final yr. Median residence costs in Cincinnati rose 12%, the third-highest enhance of all metros analyzed.

However the large story in these Ohio metros is an absence of availability. Although stock amongst all metros analyzed fell 23%, on common, in contrast with final yr, it fell 34% in Cincinnati, 33% in Cleveland and 25% in Columbus.

When evaluating this quarter’s listed houses with final quarter’s, we discover a equally dramatic lower. Cleveland noticed the biggest quarter-over-quarter dip in lively listings amongst all metros analyzed: stock fell 17% from the primary quarter. Energetic listings fell 10% in Cincinnati and seven% in Columbus on the time of yr when most markets would sometimes be flooded with residence listings.

The one factor saving consumers from being fully locked out of homeownership: affordability. So whereas discovering a house will show tough as a result of an absence of stock, houses available on the market usually tend to be inside price range for first-time consumers.

METHODOLOGY

Month-to-month median record value and record depend figures are from month-to-month Stock Knowledge from the Realtor.com residential listings database as of June 2020. The nominal record costs have been adjusted to June 2020 {dollars} utilizing the U.S. Bureau of Labor Statistics’ Client Worth Index. All month-to-month median figures have been compiled into quarterly averages.

When evaluating new quarterly knowledge with affordability knowledge within the earlier quarter, we used figures adjusted to the interval during which they have been first analyzed. For instance, first-quarter record costs and incomes weren’t adjusted to Q2 {dollars} when evaluating quarter-over-quarter modifications. This was achieved for consistency’s sake between the earlier report and the present one.

The median age of first-time residence consumers is 33, in response to the Nationwide Affiliation of Realtors’ 2019 Profile of Residence Patrons and Sellers. Estimated earnings for first-time residence consumers was derived from the U.S. Census Bureau’s 2018 American Neighborhood Survey median family earnings for homeowners ages 25-44 — the vary prone to embody most first-time residence consumers — and escalated to June 2020 {dollars} utilizing the Bureau of Labor Statistics’ Employment Value Index.

The 50 metros chosen have been up to date to mirror the newest (2019) inhabitants estimates. San Juan, Puerto Rico, is among the many 50 most populous metros however was excluded from the evaluation as a result of inadequate stock knowledge.

Interpret metro rankings with warning. Resulting from margins of error in earnings knowledge and rounding, there could also be overlap in affordability ratios.